What Is a CUSO AI Company? How CUSO Structure Changes AI Adoption for Credit Unions

Credit unions evaluating AI today face a simple question: is the company on the other side of the table built within the cooperative network, or selling into it from outside? The credit union industry has spent decades building structures that put member institutions in control of the technology and services they rely on. A new wave of AI companies is now being built inside that structure rather than outside of it, and the difference shapes everything from how decisions get made to how compliance gets handled.

This piece explains what a CUSO AI company actually is, how the CUSO model changes the economics and incentives of AI adoption, and what credit union leaders should look for when evaluating CUSO-backed AI providers.

What Is a CUSO?

A CUSO, or Credit Union Service Organization, is a company that is owned, invested in, or controlled by one or more credit unions. The structure has been a fixture of the credit union industry since the 1970s, originally created to let credit unions pool resources for back-office services like check processing, ATM networks, and shared branching.

Today, CUSOs do far more than back-office work. They build core systems, lending platforms, marketing technology, payments infrastructure, compliance tools, and now, AI. What unites them is the ownership model: credit unions are not just customers of a CUSO. They are stakeholders in it.

That distinction matters more than it sounds. When credit unions own or invest in the company building their technology, the incentives of the technology provider get pulled toward the cooperative principles credit unions operate by. The roadmap is shaped by the people who use it. The pricing is structured for credit union budgets, not enterprise bank budgets. The compliance posture is built around the regulatory environment credit unions actually face.

What CUSO AI Means

CUSO AI refers to AI companies that operate within the CUSO framework. These are AI providers that are either structured as CUSOs themselves, owned in part by credit unions or by CUSOs, or built specifically to serve the credit union market through cooperative-aligned ownership.

The category is new because AI as a serious operational tool for credit unions is new. For most of the last decade, AI in financial services was a Silicon Valley story told to enterprise banks. The technology was expensive, the implementations were complex, and the vendors were not particularly focused on the operational realities of community-sized credit unions. That is changing.

As AI moves from research to production, credit unions are finding that general-purpose AI tools do not always fit the regulatory and operational environment they work in. Compliance requirements like TCPA and FDCPA, member-facing language standards, and the workflows that connect to a credit union core all need to be handled in ways that general AI platforms were not built around. The gap between what general-purpose AI can do and what a credit union actually needs is wide enough that a new category of provider has emerged to fill it.

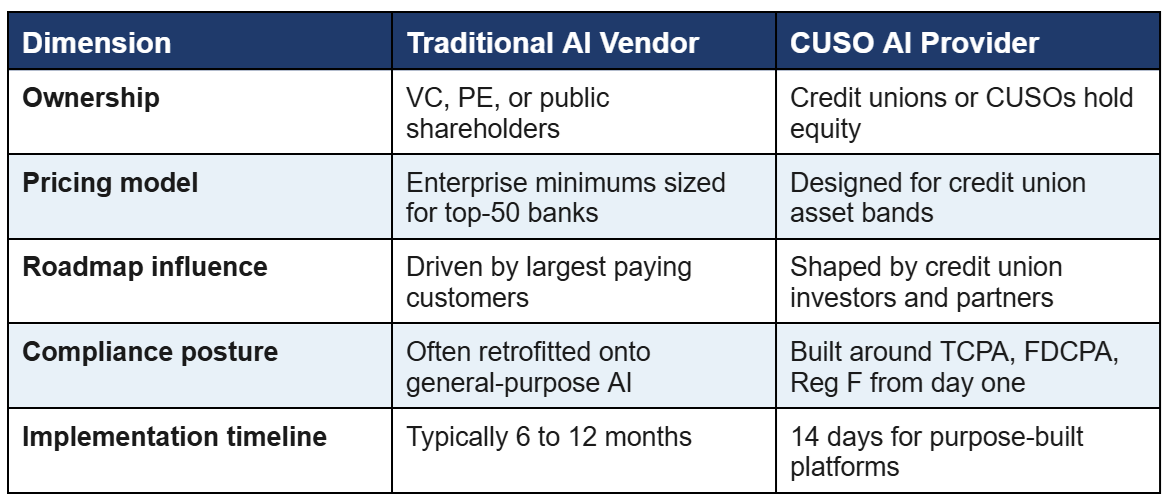

How CUSO AI Differs from Traditional AI Vendors

The structural differences between a CUSO AI provider and a general-purpose AI vendor show up in five areas:

Aligned incentives, not customer-vendor relationships

A CUSO AI company is not selling to credit unions. It is partnering with them. When credit unions are equity holders in the company building their technology, the financial alignment changes how decisions get made. Pricing structures are designed to be sustainable for credit unions of various asset sizes. Roadmap priorities are set by the people running credit unions, not by venture capital boards looking for the fastest path to enterprise revenue.

Built from inside the cooperative, not outside it

CUSO AI companies typically have founders and leadership teams that came from credit unions. That sounds like a marketing point until you sit in a product meeting with them. The conversation about how a voice agent should handle a hardship conversation lands differently when the person designing the conversation flow has spent fifteen years inside credit unions. Compliance gets built in from the start, not bolted on after a regulator raises a question.

Compliance posture matched to the regulatory environment

Credit unions live with TCPA, FDCPA, Reg F, NCUA examinations, state-by-state member privacy laws, and the operational complexity of running on cooperative principles. CUSO AI companies are built around that environment. Private LLMs, full audit trails, SOC 2 Type II, consent management, and DNC compliance are baseline requirements, not roadmap items. AviaryAI's compliance and security architecture is one example of how this gets implemented in practice.

Pricing structures designed for credit union budgets

Enterprise AI vendors selling into top-50 banks regularly quote six-figure minimums and 12-month implementation timelines. That math does not work for a $500M credit union. CUSO AI providers tend to price by usage, deploy in weeks rather than months, and require minimal IT involvement on the credit union side. The economic model is built for the institution that actually exists, not the one a sales team wishes existed.

What CUSO AI Adoption Looks Like for Credit Union Operations

The structural advantages of CUSO AI translate into specific operational realities. Credit unions working with CUSO-backed AI providers consistently report differences in how decisions get made, how quickly issues get resolved, and how the relationship evolves over time.

Faster decision cycles

When the company building your technology has credit union investors at the table, product decisions move on credit union timelines rather than enterprise software cycles. A feature request that would sit in a backlog for a year at a general-purpose AI vendor often makes the next quarterly release. Issues that would route through three layers of enterprise account management get resolved directly with the team that built the feature.

Support that speaks your language

Customer success and engineering teams at CUSO AI providers typically include people who have worked inside credit unions. When you call about a TCPA edge case or a Symitar integration question, you are not explaining your industry to the person on the other end. That difference compounds over hundreds of small interactions, and it shows up in resolution times and in the quality of the help you get.

Roadmap influence

CUSO governance structures typically include credit union advisory boards, partner councils, or direct investor representation. Your priorities have a real channel to product decisions. At a typical AI vendor, your priorities compete with whatever the largest paying customer wants, which usually means you wait.

Long-term alignment, not vendor churn

When credit unions are equity holders, the company building your technology is structurally incentivized to keep credit unions successful over decades, not to optimize for the next quarterly venture board meeting. That changes how relationship escalations get handled, how renewals get priced, and how product investments get prioritized. The relationship is built to last, because the structure rewards staying.

Why CUSO AI Is Emerging Now

Three forces are pushing CUSO AI forward at the same time.

The first is the compliance gap in general-purpose AI. Tools like ChatGPT and Claude are remarkable, but they were not built for regulated financial services. Credit unions cannot deploy them for member-facing work without serious compliance engineering. CUSO AI fills the gap by purpose-building for the regulatory environment from day one.

The second is the trust deficit between credit unions and Big Tech. Credit unions have spent generations differentiating themselves from large institutions by being closer to their members. Handing member conversations to a generic AI vendor with no credit union context runs against that positioning. A CUSO-backed provider is, structurally, part of the cooperative network rather than an outside force operating in it.

The third is the acceleration of AI adoption pressure. Credit unions that ignored AI in 2022 and 2023 cannot ignore it in 2026. Member expectations have shifted, competitor banks are deploying AI for member-facing work, and operational efficiency questions are getting harder to defer. CUSO AI is emerging as the path that lets credit unions adopt AI without abandoning the cooperative model that defines them.

How to Evaluate a CUSO AI Provider

If you are a credit union executive evaluating CUSO AI options, the right questions go beyond the demo. For a deeper buyer's framework, see our guide on how to evaluate contact center AI vendors. The CUSO-specific questions to layer on top:

- Who are the strategic investors? Are real credit unions or CUSOs on the cap table, or is it venture capital with a CUSO label?

- What is the founder's credit union background? A founder who worked inside a credit union for ten years brings different judgment than a tech founder who learned the industry through customer calls.

- How is compliance built? TCPA, FDCPA, Reg F, audit trails, private LLMs, SOC 2 Type II. These should be baseline, not future-state.

- What does the pricing model assume about your size? If the floor is set for $5B credit unions, the math will not work for most institutions.

- How long does deployment actually take? Two-week deployments are now possible for purpose-built voice AI. Twelve-month projects are usually a sign the vendor is fitting an enterprise product into a credit union shape.

- How is the roadmap shaped? Ask who decides what gets built next. If the answer is a venture board, the priorities will pull toward the highest-paying customers. If credit union leaders shape the roadmap, your needs are more likely to be heard.

AviaryAI: A Worked Example

AviaryAI is structured as a CUSO with strategic investment from Skyla Credit Union, Envisant, Encurage Financial Network, and BCU. The company was founded by Blesson Abraham, who spent 15+ years inside credit unions, including five years at BCU, and previously founded SavvyIntel (acquired by TruStage in 2017). The team has made over 4 million outbound calls for credit unions and financial institutions, with a 42% contact rate, which is 174% above the national average for outbound financial services calls.

The platform focuses specifically on outbound AI voice agents, the calls credit unions should be making but do not have the capacity to reach: collections outreach, loan servicing reminders, new member onboarding, card activation, dormant account reactivation, and proactive engagement. The CUSO structure shapes everything from how pricing is set to how compliance is built into every conversation.

AviaryAI is one example of what CUSO AI looks like in practice. There will be more. Credit unions evaluating AI in 2026 should ask whether the company they are talking to is built within the cooperative network or selling into it from outside.

Frequently Asked Questions About CUSO AI

What is a CUSO?

A Credit Union Service Organization (CUSO) is a company owned, invested in, or controlled by one or more credit unions. CUSOs provide services that credit unions could not efficiently build alone, ranging from core processing to lending technology to compliance tools. The structure has existed since the 1970s and is regulated under NCUA rules for federal credit unions.

What is CUSO AI?

CUSO AI refers to artificial intelligence companies operating within the CUSO framework. These are AI providers that are either structured as CUSOs themselves, owned in part by credit unions or CUSOs, or built specifically to serve the credit union market through cooperative-aligned ownership. The category emerged as credit unions began adopting AI for member-facing operations and found that general-purpose AI vendors did not fit the regulatory and cultural environment of credit unions.

How is a CUSO AI company different from a regular AI vendor?

Three differences stand out. First, ownership: credit unions are equity holders in CUSO AI companies, not just customers. Second, alignment: pricing, roadmap, and compliance are shaped by credit union priorities. Third, expertise: CUSO AI companies are typically founded by people who worked inside credit unions, so they understand TCPA, member experience, MSR workflows, and the cooperative model from direct experience.

Are CUSO AI companies regulated differently?

CUSOs operate under specific NCUA rules for federal credit unions, including disclosure and audit requirements. CUSO AI companies face the same baseline data security and compliance requirements as any vendor handling member data, including SOC 2 Type II, TCPA compliance, FDCPA and Reg F for collections work, and state privacy regulations. The CUSO structure does not exempt the company from any of these. It does change who is accountable when decisions get made about how the technology evolves.

Can community banks use CUSO AI providers?

Yes. CUSO AI providers typically serve credit unions first because of structural alignment, but the technology and operational expertise also apply to community and regional banks. Many of the same compliance requirements (TCPA, FDCPA, Reg F, SOC 2) apply across credit unions and community banks. The conversation flows, integration approach, and use cases translate well between the two.

Who are the major CUSO AI providers today?

The category is still forming. AviaryAI is one example, structured as a CUSO with strategic investment from Skyla, Envisant, Encurage, and BCU, focused on outbound AI voice agents. Other CUSOs are building AI capabilities into existing service offerings (lending tech, marketing automation, compliance tools). Expect this list to grow significantly over the next 24 months as AI adoption accelerates and more cooperative-aligned providers emerge.

What is the difference between CUSO AI and AI for credit unions?

Any AI vendor can claim to serve credit unions. The CUSO designation reflects ownership structure: credit unions or CUSOs hold equity in the company. An AI vendor that markets to credit unions but is owned entirely by venture capital or private equity is not CUSO AI, even if its product works well for credit unions. The structural difference matters because it shapes incentives over the long term.

• • • • • • •

See What CUSO-Backed AI Looks Like in Practice

AviaryAI is built within the credit union network, not outside it. CUSO-backed, founded by credit union veterans, and proven across 4 million+ outbound calls.

Book a Demo | Hear an Agent at Work